With the European Central Bank (ECB) cutting interest rates by 25 basis points on 6th June, 2024, the financial community is abuzz with speculation regarding when the Bank of England (BoE) will follow suit.

This potential change would reverse the rate-hiking cycle that has marked the post-lockdown years, with significant implications for investors, not least for defined benefit (DB) pension schemes, which invest heavily in government bonds – the performance of which is linked to the interest rate environment. DB schemes should therefore consider their hedging strategies and leverage levels, both to take advantage of the current rate environment and to cushion their portfolios from this impending change.

BoE’s decision-making focus

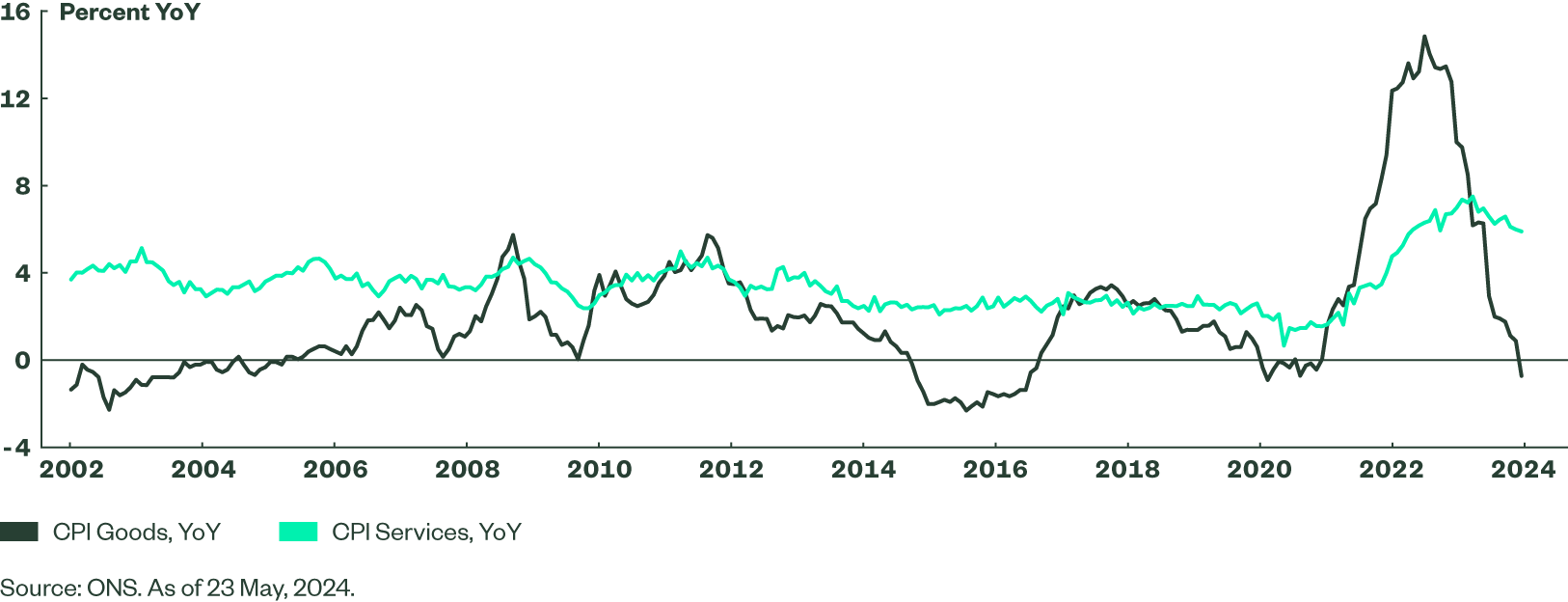

The BoE’s Monetary Policy Committee (MPC) considers many factors when making interest rate decisions, but the current focus will be on three interrelated indicators: services inflation, labour market tightness and wage growth. Though the BoE’s target is headline CPI, services inflation is a seen as a key barometer of domestic price pressures. This form of inflation has proved sticky, only gradually ticking down over the course of the past year with the latest reading at 5.9% YoY for April 2024 – significantly higher than goods inflation, which was in deflation territory in the latest reading.

Figure 1: CPI Inflation

However, labour costs are a large component of services costs, and both labour market conditions and wage growth paint a more promising picture.

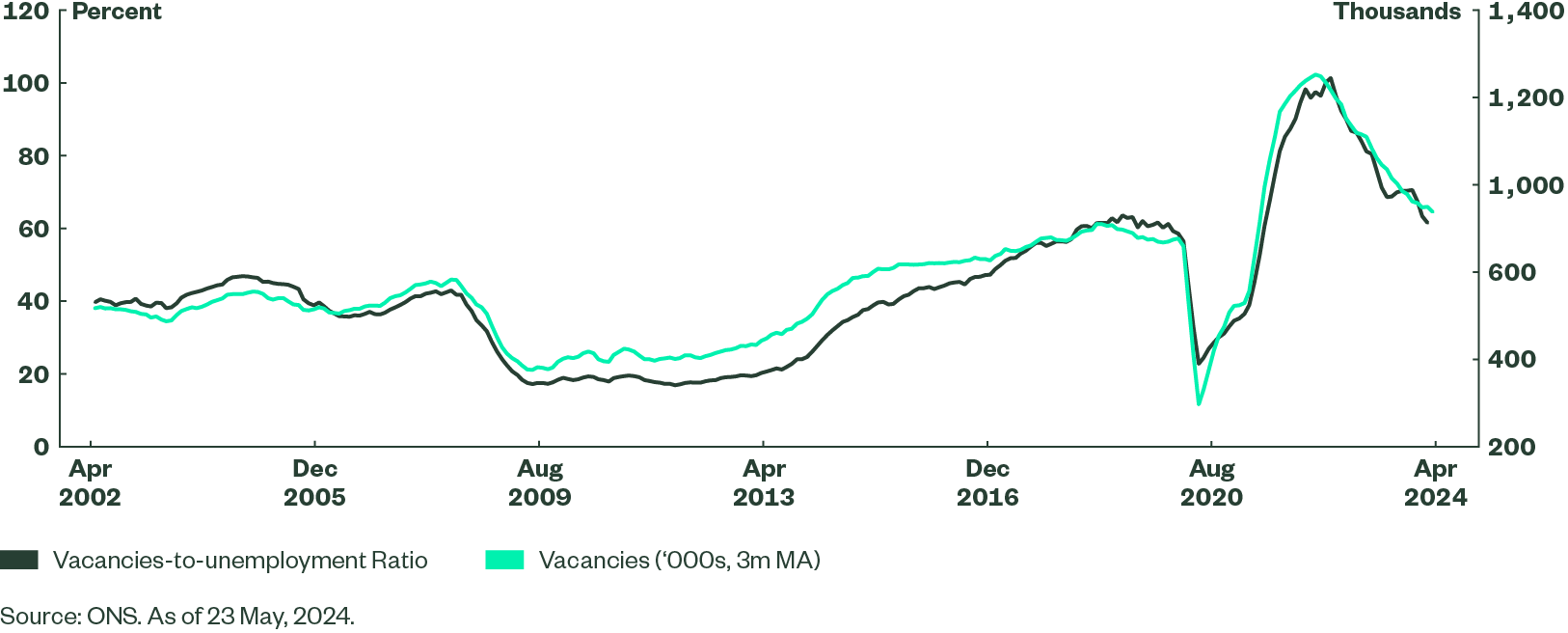

A tight labour market in economics is a situation of relative scarcity of labour supply to demand. A key metric watched by the BoE, the vacancies to unemployment ratio, shows that the UK labour market has loosened significantly since its extreme post-lockdown squeeze, see chart. However currently this is only at levels that would be considered tight before the pandemic.

Figure 2: UK Labour Market: Vacancies to Unemployment

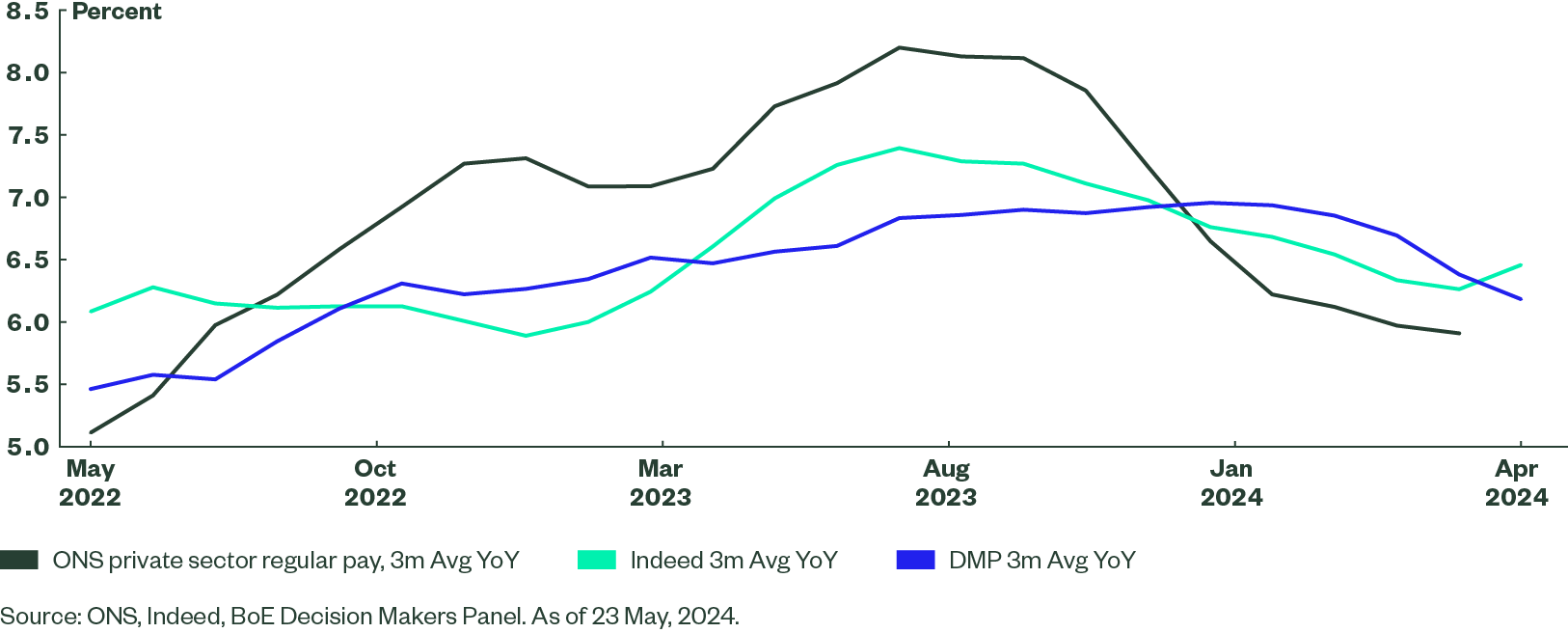

A loosening labour market has helped to slow wage growth, with the MPC’s favoured measure, private sector wage growth excluding bonuses, at 5.9% 3m YoY in March – its lowest level since June 2022. Wage growth moderation is corroborated by other indicators too. The job is not done yet though, as this is still somewhat away from a level that would be consistent with the MPC’s 2% inflation target.

Figure 3: UK Wage Growth

How many cuts will we get?

With each of these indicators in mind, it appears a cut to the UK’s Bank Rate is increasingly likely – and more members of the MPC seem to agree.

At the MPC’s meeting in March, no members voted to raise the Bank Rate for the first time since the hiking cycle began. Then, in May, Sir Dave Ramsden joined Dr Swati Dhingra in voting for a rate cut.

Amy Le, within SSGA’s Economics team, expects to see at least two rate cuts this year given that growth is gradually picking up whilst the jobs market is cooling. In addition, as the surge in April’s cost pressure, which is related to the 10% rise in the National Living Wage, is showing signs of easing in May, particularly in the services sector, this would strengthen the probability of a first rate cut in August. Find out more in our economics team’s recent blog: Central Bank Check-In: What’s Next Around the Globe

Implications for DB schemes

As government bond yields typically decline as central banks cut interest rates, DB pension schemes should consider further increasing the level of interest rate hedging within the scheme, both to take advantage of the current level of government bond yields and to protect themselves against future declines in yields.

Pension schemes that have gained leverage using repos within their pension schemes will directly benefit from cuts to Bank Rate as this reduces the cost of borrowing within their LDI fund. In addition, should longer dated bond yields decline alongside cuts in Bank Rate, pension schemes will benefit from an increase in the value of their collateral, which will allow them to potentially reduce the level of leverage within the scheme.

Strategic considerations for DB pension schemes

Given the potential for rate cuts by the BoE, it’s crucial for schemes to reassess their hedge ratios – the extent to which their liabilities are protected against interest rate movements.

State Street Global Advisers (SSGA) offers a compelling proposition in this regard, with custom LDI strategies that help ensure schemes are protected from the impacts of rate cuts and poised to capitalise on market opportunities.

Our clients benefit from:

-

Service-led approach: SSGA’s LDI proposition comes with an enhanced level of service, offering tailored support and quick access to both experts and data.

-

Improved reporting: We offer daily LDI portfolio valuation and analytics reports, tailored to suit the needs of our clients and their advisers.

-

Lower fees: SSGA’s proposition emphasises cost-effectiveness, enabling schemes to benefit from low management fees. These savings can quickly offset any transition costs for schemes looking to move from another LDI provider.

-

Technology-led portfolio management: Each of these benefits is made possible by our best-in-class technology platform, the Charles River Investment Management Solution (CRIMS), which manages every aspect of our LDI mandates with precision and scale.

While speculation of a cut to the Bank Rate indicates a welcome return to economic normality, the upheaval associated with this policy shift may be significant. Trustees of DB schemes should work with their LDI manager and advisors to navigate this regime change and how it will impact their portfolios. Visit our website for further LDI insights.

Disclosure

Marketing communication.

For institutional/professional investors use only.

United Kingdom: State Street Global Advisors Limited. Authorised and regulated by the Financial Conduct Authority. Registered in England. Registered No. 2509928. VAT No. 5776591 81. Registered office: 20 Churchill Place, Canary Wharf, London, E14 5HJ. T: 020 3395 6000. F: 020 3395 6350.

The information contained in this communication is not a research recommendation or ‘investment research’ and is classified as a ‘Marketing Communication’ in accordance with the Markets in Financial Instruments Directive (2014/65/EU) or applicable Swiss regulation. This means that this marketing communication (a) has not been prepared in accordance with legal requirements designed to promote the independence of investment research (b) is not subject to any prohibition on dealing ahead of the dissemination of investment research.

The views expressed in this material are the views of Daoyu Chen, CFA, Senior Investment Strategist through the period ended 6 June, 2024 and are subject to change based on market and other conditions. This document contains certain statements that may be deemed forward-looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected.

The trademarks and service marks referenced herein are the property of their respective owners. Third party data providers make no warranties or representations of any kind relating to the accuracy, completeness or timeliness of the data and have no liability for damages of any kind relating to the use of such data.

The information provided does not constitute investment advice as such term is defined under the Markets in Financial Instruments Directive (2014/65/EU) and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell any investment. It does not take into account any investor’s or potential investor’s particular investment objectives, strategies, tax status, risk appetite or investment horizon. If you require investment advice you should consult your tax and financial or other professional advisor.

This communication is directed at professional clients (this includes eligible counterparties as defined by the appropriate Financial Conduct Authority (FCA)) who are deemed both knowledgeable and experienced in matters relating to investments. The products and services to which this communication relates are only available to such persons and persons of any other description (including retail clients) should not rely on this communication

Investing involves risk including the risk of loss of principal. Past performance is no guarantee of future results.

The whole or any part of this work may not be reproduced, copied or transmitted or any of its contents disclosed to third parties without SSGA’s express written consent.

All information is from SSGA unless otherwise noted and has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such.

Information Classification: General6676234.1.1.EMEA.INSTExpiry: 31/05/2025© 2024 State Street Corporation - All Rights Reserved.