Analysis: Pension schemes continue to pour assets into fast-growing alternative risk premium strategies, despite a torrid 2018 for returns and concerns over the diversification benefits delivered by the funds.

Consultancy MJ Hudson now estimates the size of the ARP market at between $150bn (£115.2bn) and $200bn, up from between $100bn and $150bn a year ago despite negative average returns.

Forty-six per cent of surveyed managers saw growth of more than 20 per cent in the year, while pension funds remained by far the biggest source of assets.

ARP funds, sometimes known as alternative beta, are those that attempt to capture return-driving factors, usually in a multi-asset and market-neutral context. As such, they are distinct from cheaper ‘long-only’ smart beta funds.

They need a long investment time horizon given it can be quite a volatile strategy, which is what we have seen in 2018

Chris Pritchard, Barnett Waddingham

Despite the strategies’ growing popularity, MJ Hudson’s research shows returns have been anything but appealing over the last year.

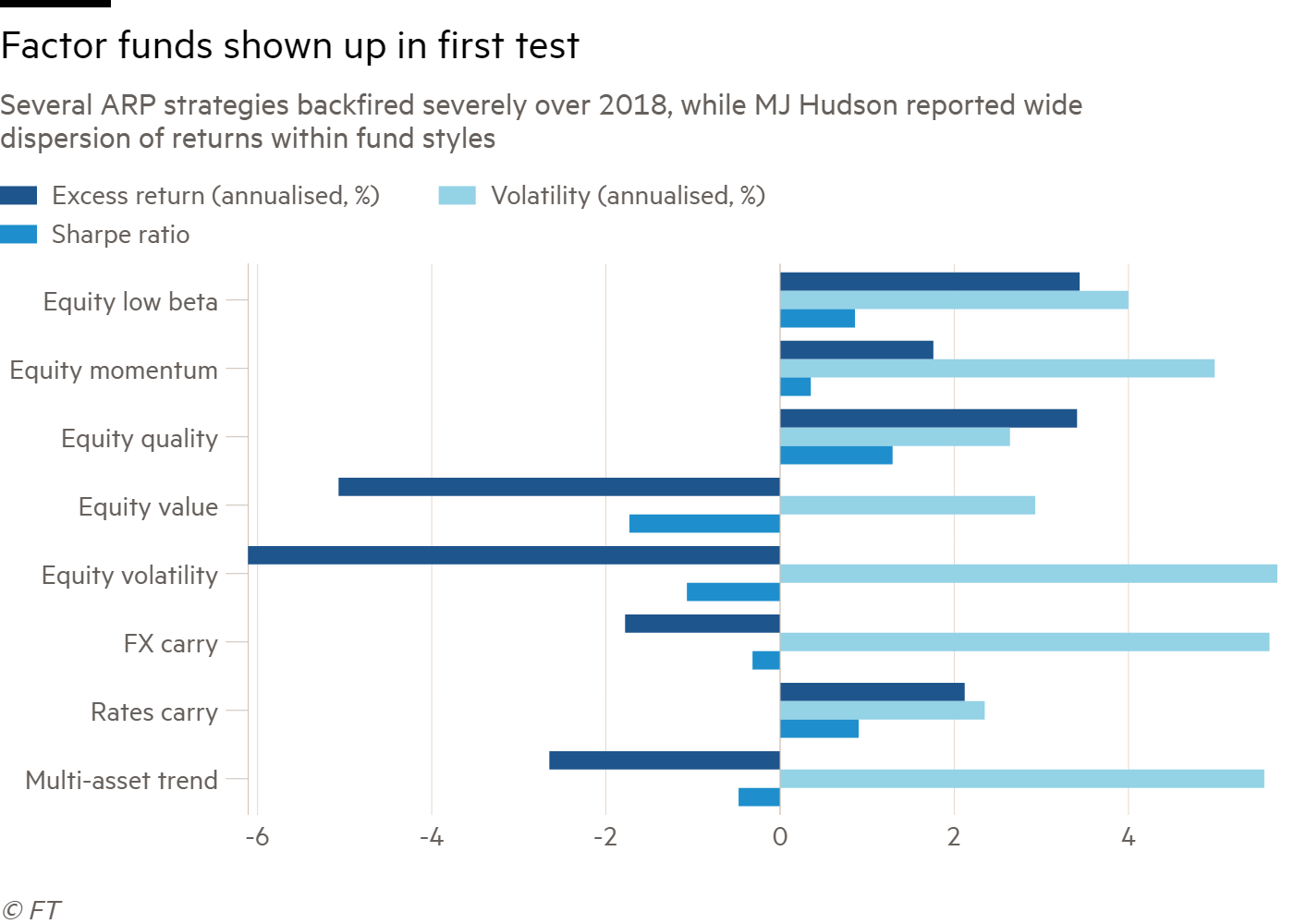

The average ARP fund lost 7.5 per cent relative to cash in 2018, with a volatility of 6.1 per cent. That figure hid a wide dispersion of performance, with the best performers generating 3.4 per cent returns and the worst losing 13.6 per cent over the year. Average fees were 0.82 per cent.

Worse, the funds, which are often sold on their low correlation with traditional asset class drivers of return, suffered drawdowns during a year of similar losses for equities.

“2018 was an important year for the industry in the sense that it was a reality check for investors,” says Antti Suhonen, director at MJ Hudson. “It’s clear that many [ARP strategies] go through extended periods of drawdown.

One such example was that set by strategies shorting equity volatility, which fell victim to the same bout of price swings that caused exchange-traded volatility products to implode spectacularly in February.

It is difficult to make generalisations about the merits of investment in ARP funds, Mr Suhonen says, because of the wide variety of investment philosophies in the sector.

MJ Hudson identified six main sources of return used in the funds, comprising several equity-related factors alongside short equity volatility, FX carry, and multi-asset trend following

On top of the disparate returns between these broad categories, Mr Suhonen says differences in implementation can yield vastly different result even within styles.

Performance generates critics

The disappointing returns, cost and complexity of the funds involved mean that some investment consultants are not prepared to recommend them to clients.

“We don’t really buy into them,” says Ben Gold, head of investment for Leeds at XPS Pensions, doubting factor investments’ ability to add value.

Mr Gold says his focus is on helping clients achieve diversification away from equity markets via assets such as those with contractual cashflows, or exploiting illiquidity premiums.

“We just think that’s far easier to understand, far clearer how the returns are going to be delivered than things like the alternative risk premia.”

Trustees must be prepared for losses

Certainly, trustee boards must be well informed about the complexities of the asset class before investing. Chris Pritchard, investment actuary at Barnett Waddingham, says that for ARP to be appropriate, clients must have sufficient knowledge of the asset class, already have diversified exposure to traditional assets and be prepared to wait out periods of losses, he said.

“They need a long investment time horizon given it can be quite a volatile strategy, which is what we have seen in 2018,” he says.

However, Mr Pritchard questions whether poor 2018 performance signals correlation with equities or merely coincidence, noting that drawdowns in the two occurred at different times in the year.